Tattersalls Rule 4 Mathematics: Calculating Late Withdrawal Deductions

The first time I lost money to a horse I never even backed, I was nineteen and standing in a Ladbrokes in north London. My selection had won at 5/2, returns should have been £35, and the cashier handed me £32.50. He pointed at a card pinned above the till – Rule 4(c), Tattersalls Committee, 7.5p in the pound – and shrugged. That was twenty-something years ago, and I have been explaining the same shrug to friends, colleagues and bewildered relatives ever since.

Rule 4 is a Tattersalls Committee rule. Tattersalls is the private body that has settled betting disputes in Britain for the best part of two centuries, and Rule 4(c) is the specific clause that allows bookmakers to deduct from your winnings when a rival horse is withdrawn from the race after the market has been set. The penny-in-pound scale is fixed, the timing is mostly predictable, and the maths is not difficult once you have seen it twice. But almost nobody explains it before you have already lost money to it, which is why I keep coming back to this subject. If you bet on British racing in 2026 – fixed-odds, multiples, even some ante-post bets – Rule 4 will touch your slip sooner or later.

What follows is the table, the timing, the worked numbers and the edge cases. By the end you should be able to look at a withdrawn horse, read its starting price in the morning paper, and tell me before the off how much smaller your win will be.

The Tattersalls Table, Read Line by Line

Rule 4(c) deductions are scaled to the odds of the withdrawn horse at the time it was taken out of the race. That is the only number that matters. The bigger the withdrawn horse was fancied, the more your returns get cut. The logic is mechanical: if a 4/6 favourite is scratched, the rest of the field shortens dramatically, so the bookmaker reduces your effective price to keep the book honest.

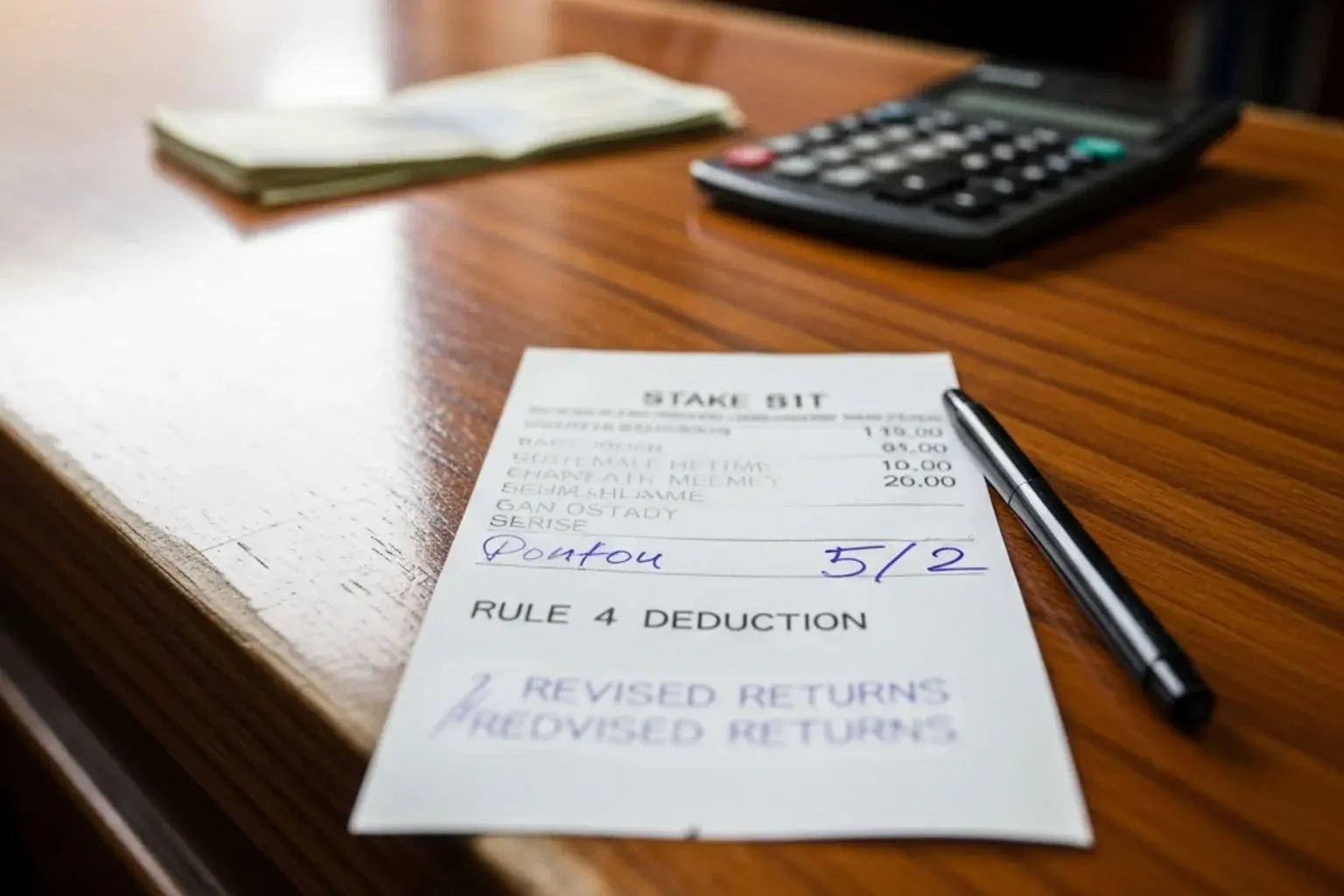

The scale, in the form every UK on-course bookmaker and high-street settler has memorised, runs from a token deduction at long prices up to a swingeing 90p in the pound on odds-on shots. The shape worth remembering: 1/9 or shorter, 90p; 2/11 to 2/17, 85p; 1/4 to 1/5, 80p; 3/10 to 2/7, 75p; 2/5 to 1/3, 70p; 8/15 to 4/9, 65p; 8/13 to 4/7, 60p; 4/5 to 4/6, 55p; 20/21 to 5/6, 50p; evens to 6/5, 45p; 5/4 to 6/4, 40p; 13/8 to 7/4, 35p; 15/8 to 9/4, 30p; 5/2 to 3/1, 25p; 10/3 to 4/1, 20p; 9/2 to 11/2, 15p; 6/1 to 9/1, 10p; 10/1 to 14/1, 5p; and over 14/1, no deduction at all.

Two practical points. First, the deduction is applied to your winnings – your profit – not to your total returns. Get that wrong and your mental maths will be miles off. Second, when the bookmaker chalks up the percentage in the shop or shows it on the bet slip, they are quoting the deduction itself, not what is left. A notice of “Rule 4 – 25p in the £” means your winnings will be paid at 75 per cent of face value. The headline is the loss, not the survival.

The scale was last meaningfully revised in 2003 and has held ever since. It is one of the few pieces of British betting infrastructure that has outlasted every wave of digital migration, every Levy reform, every Gambling Commission consultation. The settlers’ shorthand at on-course books still reads exactly the same as it did when I was a kid leaning over a rope at Sandown.

When Rule 4 Applies and When It Quietly Does Not

The trigger is straightforward: a horse must be declared, the market must be open, and the horse must then be withdrawn before the off. Withdrawal after declaration but before the race – that is the Rule 4 window. The clock starts the moment the bookmaker frames a price; it ends when the runners come under starter’s orders. Outside that window, the rule does not bite.

Ante-post bets sit outside, in the main. If you took 25/1 about a Grand National horse in February and it never makes the line-up in April, an ante-post bet without the NRNB concession is simply a loser – your stake is gone, and no Rule 4 enters the picture, because no rival was withdrawn from a settled market in which you held a price. Non-runner-no-bet markets work differently and have their own settlement language; I cover that in how non-runner no bet reshapes ante-post punting.

Where things get awkward is in the morning of the race itself. Modern fixed-odds markets reopen at first show, usually around 8am. If you took an early price at 7/1 at 8.30am and a 7/4 favourite is then withdrawn at 10am because of a vet’s report, Rule 4 applies to your 7/1 ticket. The deduction is calculated from the price of the withdrawn horse at the moment of withdrawal – not yesterday’s ante-post quote, not the morning paper’s tissue, not the price you took. Your bookmaker uses their own internal record of the prevailing price at withdrawal. On-course, the same principle applies, but the rule is more visible: the bookmaker physically rubs the horse off the board and chalks the deduction next to the race name.

Race-day timing has tightened in recent years. In 2025 only 82.2 per cent of British races started within two minutes of their scheduled time, up from 72.7 per cent two seasons earlier – a sharp improvement that owes a great deal to BHA pressure on stalls handlers, stewards and vets. The tighter the schedule, the smaller the window for late withdrawals, and the rarer Rule 4 becomes on any individual race. But total betting turnover on British racing has fallen nine per cent year on year through 2025, with the BHA’s Director of Racing noting that there is wider work to be done on the racing product as a betting medium. None of that softens Rule 4 when it lands on your slip.

Worked Examples From the Slip

Numbers fix this in the mind faster than words ever will. Take the £10 win bet at 5/2 that opened this article. Returns at face value: £25 winnings plus £10 stake equals £35. A 7/4 second favourite is withdrawn after declaration, triggering a 25p deduction. The bookmaker takes 25 per cent off the £25 winnings – £6.25 – leaving £18.75 of profit. Total returns: £28.75, not £35. Tuck that maths somewhere you will not lose it: the deduction shaves your profit, the stake comes back untouched.

Now try a slightly steeper one. A £20 win bet at 4/1 with a 5/6 favourite scratched on the morning of the race. The 5/6 sits in the 55p band. Face-value winnings of £80 become £36 after the 55 per cent cut. Returns: £56. The deduction has nearly halved what you stood to win, which is exactly why the on-course men used to call out Rule 4 in capital letters whenever a fancied horse came out of a small field.

One more. A £5 each-way bet at 12/1, 1/5 odds for four places, with a 2/1 third favourite withdrawn at 1.45 for a 2.10 race. The 2/1 sits in the 30p band. The win side: £60 winnings face value, 30 per cent off – £42 winnings, returns £47. The place side: 12/1 at 1/5 means a place price of 12/5, or 2.4/1; face-value place winnings of £12 become £8.40, returns £13.40. Total returns from a £10 stake: £60.40, against face-value returns of £77. The deduction does not double up – it applies once across both halves of the each-way, calculated from the same withdrawn price. If you bet on the Aintree fixture in 2025 – the meeting alone took roughly £200 million in stakes, with Grand National Saturday accounting for the bulk – there were dozens of slips like this circulating across the country. Most punters never saw the maths, only the smaller payout.

Multiple Withdrawals and the Stacking Question

Field sizes have shrunk. Britain had 18,452 horses run at least once in 2024, down one per cent on 2023 and continuing a roughly 1.5 per cent annual decline since 2022. Smaller fields mean withdrawals bite harder; they also mean more than one horse coming out of a race more often than I remember from the early 2000s.

The stacking rule is simple: deductions are cumulative, capped at 90p in the pound. If a 2/1 shot is withdrawn at midday and a 4/1 shot at 1.30, the deductions are 30p plus 20p, totalling 50p – your winnings are halved. If a third horse goes at 3/1, that is another 25p, and the cap kicks in: a maximum 75p has been deducted in total. The cap stops the rule from ever wiping out winnings entirely; the bookmaker always pays something, even on a Tuesday afternoon novice hurdle with three late vet’s certificates. The maths in practice is straightforward: total the percentages, apply the total to your winnings, return the stake whatever happens. The same principle holds on each-way and on every leg of a multiple – if any leg of an accumulator contains a Rule 4, that leg is settled at the reduced price before being multiplied through. I have seen Lucky 15s with two Rule 4 legs that still paid out a small bonus, and I have seen accumulators die from a single 90p deduction that turned a 50/1 shot into a token return. The rule survives every market shift because the alternative – voiding bets every time a vet pulls a horse out – would be unworkable for any bookmaker running a balanced book.